Farmland is one of the few assets that produce something essential: food, fuel, and fiber. It’s a real, tangible resource with intrinsic value, yet often overlooked as an investment.

Today, that’s starting to change. As access improves through platforms like AcreTrader, more investors are taking a closer look at farmland not just as real estate, but as a long-term asset class shaped by a few simple, durable forces: limited supply, steady demand, and consistent income potential.

A Finite Asset in a Growing World

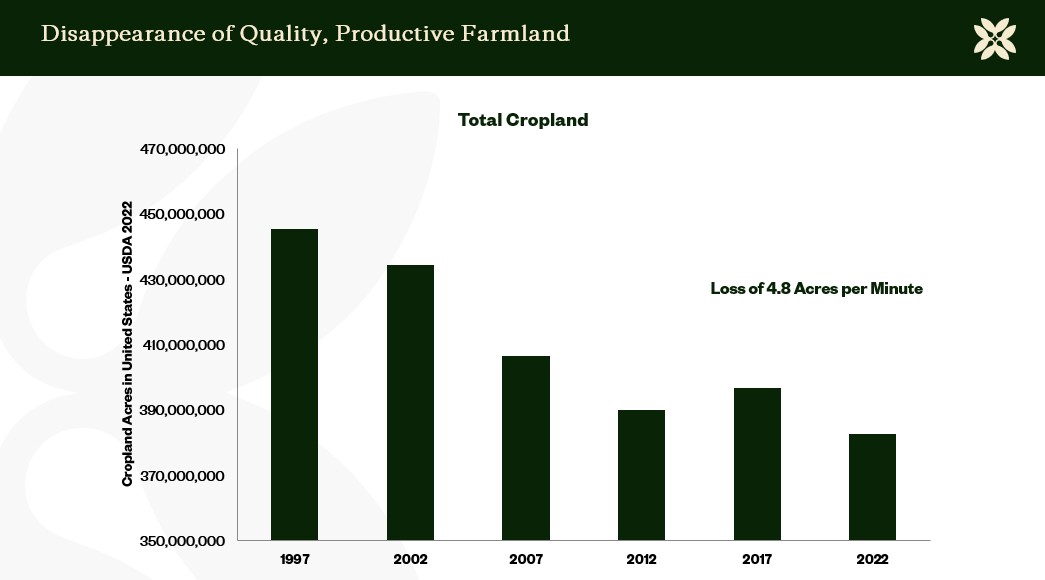

The most important driver of farmland value is also the most straightforward: there isn’t much of it, and there’s less every year. In fact, USDA data shows the United States loses 4.8 acres of cropland every minute.

Figure 1

In the U.S., millions of acres of cropland have been lost to development, infrastructure, and other competing land uses. High-quality farmland, especially in core growing regions, is even more limited. And unlike other asset classes, you can’t simply create more of it.

At the same time, demand continues to rise. Global population growth, shifting diets, and increasing pressure on food systems all require more agricultural output. That dynamic, shrinking supply paired with steady or growing demand, has historically supported long-term farmland appreciation.

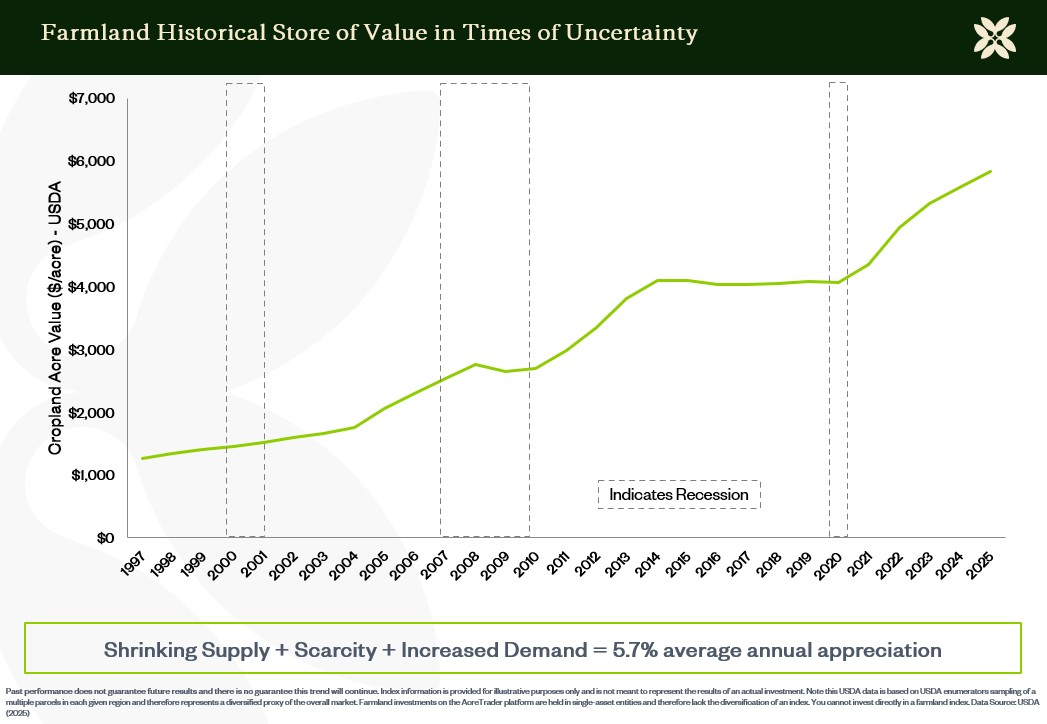

Why Farmland Doesn’t Follow Typical Market Cycles

Most asset classes respond to capital flows. When prices rise, more capital enters the market, supply increases, and returns eventually normalize.

Farmland doesn’t work that way, as no amount of capital can economically increase the supply of high-quality farmland.

Figure 2

Built-In Income with Low Vacancy Risk

Farmland also generates income, typically through leasing to farmers.

Unlike many forms of real estate, productive farmland has effectively zero vacancy risk. Farmers need land to operate, and high-quality acreage is consistently in demand. As a result, most farmland is continuously leased, providing predictable annual cash flow.

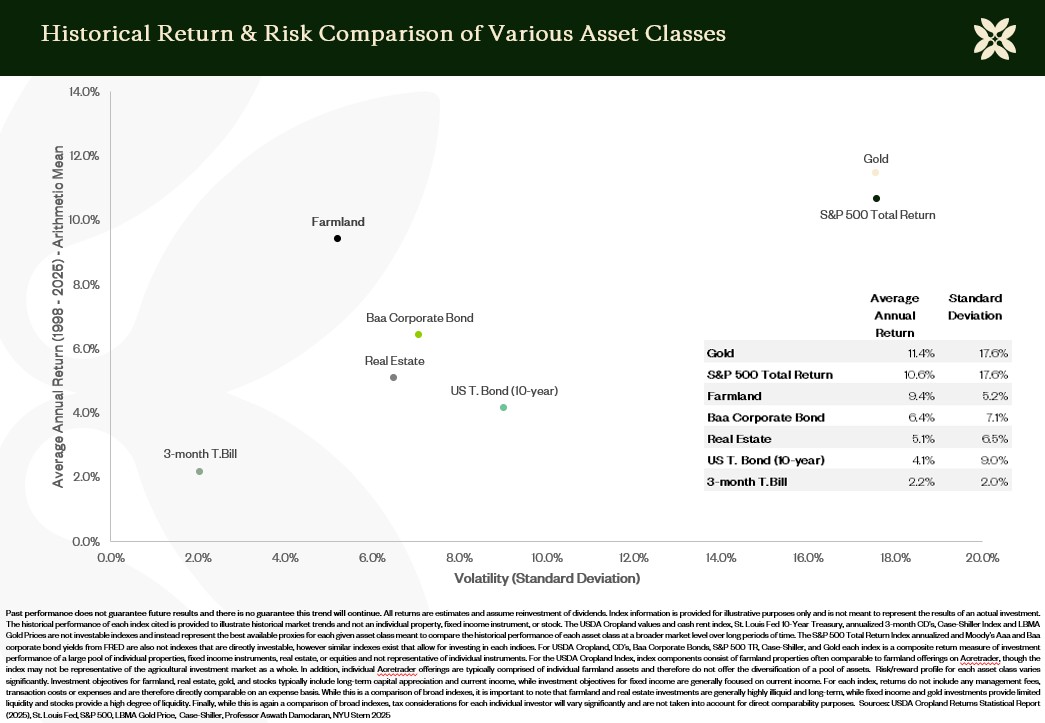

When combined with farmland appreciation, this has historically resulted in relatively attractive returns vs. other asset classes with limited volatility. This combination of income and appreciation is central to farmland’s appeal.

Resilience Through Market Stress

In the last 3 years, the resiliency of farmland values has been significantly tested, and the results are telling. For example, corn, soybean, and cotton prices peaked in Q2 2022 and subsequently fell 50% (corn), 40% (soybeans), and 60% (cotton). In addition, input costs such as fertilizer, herbicides, and diesel prices have increased significantly since 2022. Finally, interest rates increased at the fastest pace in history, driving ag operating lines of credit rates ~3x higher. Despite these headwinds, cropland values according to the USDA increased 18% from June 30, 2022 to June 30, 2025. Farmland indices such as Purdue University's and ISPFMRA show similar trends. This highlights the importance of supply-and-demand dynamics for farmland and how they differ from those in the broader production ag economy.

That consistency is a key reason investors view farmland as a long-term store of value rather than a short-term trade.

This disconnect highlights an important point: farmland values are not solely tied to short-term farm economics. Instead, they are more heavily influenced by long-term supply-and-demand fundamentals. Even during periods of stress in the broader agricultural economy, the underlying asset—land—has historically held its value.

Figure 3

A Natural Hedge Against Inflation

Farmland has also shown a strong historical relationship with inflation.

As the cost of goods rises, particularly food, so does the value of the land that produces it. Over long periods, farmland returns have been positively correlated with inflation, meaning it has tended to perform well when inflation is elevated.

This becomes especially important when traditional diversification strategies fall short. In periods of higher inflation, stocks and bonds have historically moved more closely together, reducing the effectiveness of a standard 60/40 portfolio.

Farmland, as a real asset, has behaved differently, often maintaining low or negative correlation to financial markets and helping diversify overall portfolio risk.

Farmland isn’t a new asset class, but it is newly accessible.

At its core, the investment case is simple: a finite resource, steady demand, consistent income, and a history of resilience. These fundamental drivers have shaped farmland performance for decades and remain true today.

For investors looking beyond traditional markets, farmland offers something increasingly hard to find: real assets with real utility, grounded in long-term fundamentals rather than short-term cycles.

By Drew Lipke, Managing Director at AcreTrader